What's Inside a Level-Funded Health Plan?

Get Out-Of-Pocket in your email

Looking to hire the best talent in healthcare? Check out the OOP Talent Collective - where vetted candidates are looking for their next gig. Learn more here or check it out yourself.

Hire from the Out-Of-Pocket talent collective

Hire from the Out-Of-Pocket talent collectiveHealthcare 101 Crash Course

%2520(1).gif)

Featured Jobs

Finance Associate - Spark Advisors

- Spark Advisors helps seniors enroll in Medicare and understand their benefits by monitoring coverage, figuring out the right benefits, and deal with insurance issues. They're hiring a finance associate.

- firsthand is building technology and services to dramatically change the lives of those with serious mental illness who have fallen through the gaps in the safety net. They are hiring a data engineer to build first of its kind infrastructure to empower their peer-led care team.

- J2 Health brings together best in class data and purpose built software to enable healthcare organizations to optimize provider network performance. They're hiring a data scientist.

Looking for a job in health tech? Check out the other awesome healthcare jobs on the job board + give your preferences to get alerted to new postings.

TL;DR

Level-funding is a type of health coverage that small businesses can offer their employees. It allows businesses to get underwritten differently, save money if their employees expenses are lower than predicted, and give more flexibility for how they design coverage.

We walk through what level-funding is and the component pieces. Arlo is a level-funded health plan for small businesses that bundles everything end-to-end: underwriting, stop loss, TPA, PBM, network, and care navigation.

We go under the hood to see how they make money and what’s included in their plans. We’ll talk about the innovation that’s happening in the small group space, and some of the practical and ideological challenges they might encounter as they grow.

This is a sponsored post. You can read more about my rules/thoughts on sponsored posts here.

–

Company Name - Arlo

The company is called Arlo. They create level-funded plans for small groups. They join the other payers just mashing two normal sounding words together for some reason.

The company started by helping insurers underwrite small groups, but eventually started taking on that underwriting risk themselves and administering the plans.

They’re putting the fun in level-funded, which isn’t really fun at all so idk.

What's the Pain Point?

If you're a company with like 40 employees and want to offer insurance, you can get small group insurance from a health insurance carrier. You usually get some choices in options, but this product has been getting particularly expensive. Its premiums multiplied by # of employees, and you basically just get a bill. No information on where the spend was, benefits for containing healthcare costs, etc. Might as well just add the 20% tip screen at that point.

This is a "fully insured"arrangement - the business pays premiums to a health insurance company, and the insurer takes on the financial risk. If one employee gets a $500K cancer diagnosis, the insurer pays for it.

In the past, we’ve talked about how these fully insured groups are underwritten using an approach called "modified community rating” to figure out the premiums an employer will pay. Insurers can only adjust prices based on a few factors like age and geography instead of the health and expenses of employees. Personally, I think they should make anyone in the 10016 zip code pay triple on principle, but that’s just me.

If you're a small business and your employees don’t use the healthcare system that much, you might be wondering what you’re paying for, and especially if your premiums keep going up. So, you might start looking for cheaper options.

Large employers do this by self-funding. This is where the company itself pays for employee healthcare costs directly. They can underwrite based on actual risk and customize their plan however they want. But self-funding as a 20-person company is terrifying because one really expensive employee could bankrupt you.

So a newish product has emerged called level-funding, which is designed for smaller employers. More than a third of small firms that offer coverage are now in one of these arrangements.

What Is Level-Funding?

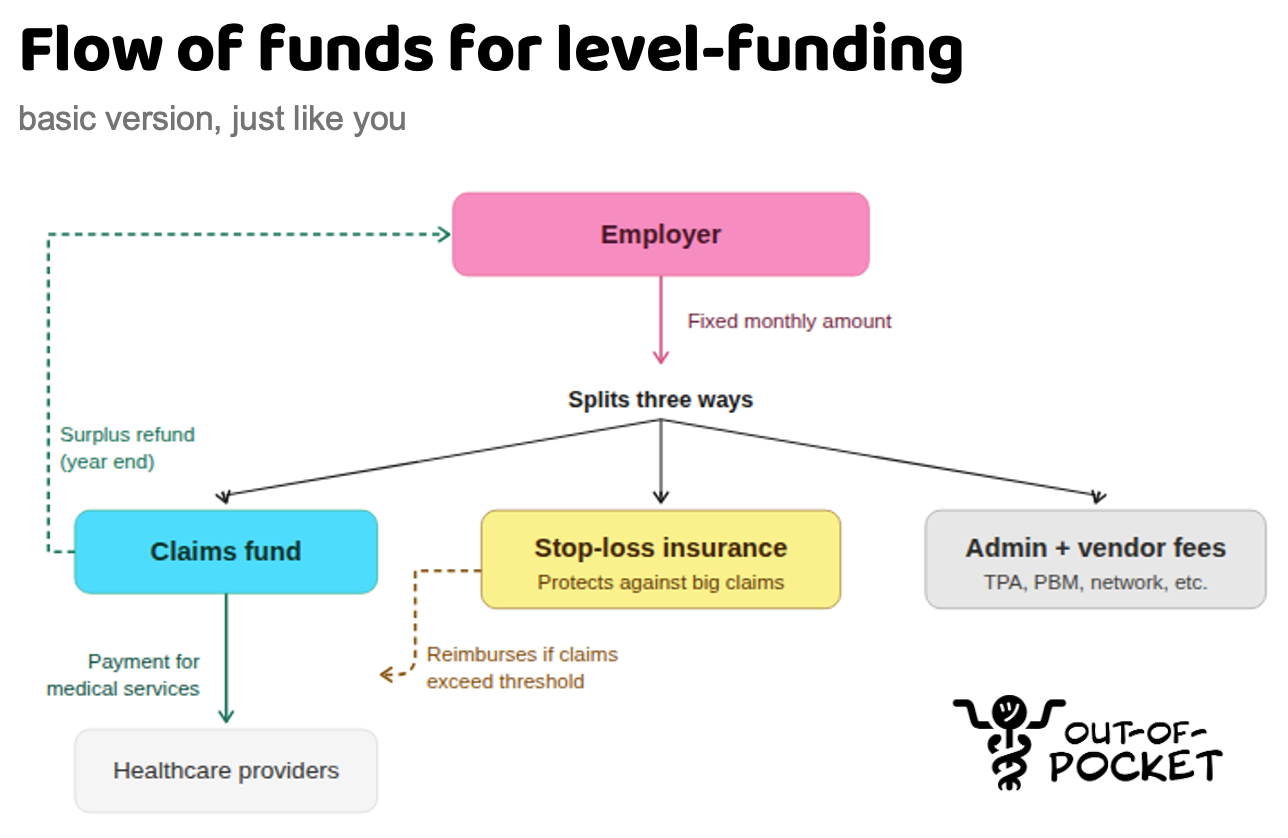

Here are the basics of level-funding. Every month, the employer pays a fixed amount that looks kind of like a premium. That money gets split three ways:

1. Claims fund - This is the pot that actually pays for employees' medical costs, the one guarded by the leprechaun.

2. Stop loss insurance - This protects the employer if a massive bill hits. This could be one patient getting really expensive, or a bunch of people getting smaller procedures that add up. If you blow past a certain amount in medical expenses, the stop loss carrier picks up the tab.

3. Vendor and admin fees - This is for all the stuff that makes the plan actually run: the third-party administrator that processes claims, the pharmacy benefits manager that handles prescriptions and drug coverage, the network, the decorative provider directory, care navigation, etc.

There are three big features to level-funding if you’re an employer.

The first is that the underwriting is different. I wrote a very long post about this, but essentially you can price premiums based on how medically expensive your employee pool is. If you have a healthier, less expensive pool, this works in your favor. If you don’t, you’ll likely get worse premiums. For some employers, this alone is a huge perk because the premiums come out much cheaper.

The second is that if your employees don't use all the money in the claims fund by the end of the year, you get a portion of the surplus back. This means you have an incentive to contain costs and give tools to guide employees to cheaper places.

And finally, level-funded plans are governed under ERISA instead of the Department of Insurance. This gives these more regulatory flexibility than fully-insured plans that have to follow state-by-state rules. This matters because it means level-funded plans can do things like offer the same plan design across multiple states without getting 50 different state approvals and do more creative things like:

- Waive co-pays for high performing docs

- Create direct contracts with local hospitals if you have a lot of employees in one area

- Get drugs from other countries for cheaper

- Cover GLP-1s without requiring a blood oath

Level-funding is similar to self-funding but with less volatile spend and a more vague name. In level-funding, the employer pays a fixed amount each month, vs. self-funding, where it’s dependent on whatever the medical expenses are. Self-funded employers save more money than level-funded plans if their claims end up being lower, but will lose more money if their claims are higher.

Many companies will start at level-funding and graduate to self-funding as the company gets larger. There’s…levels to this.

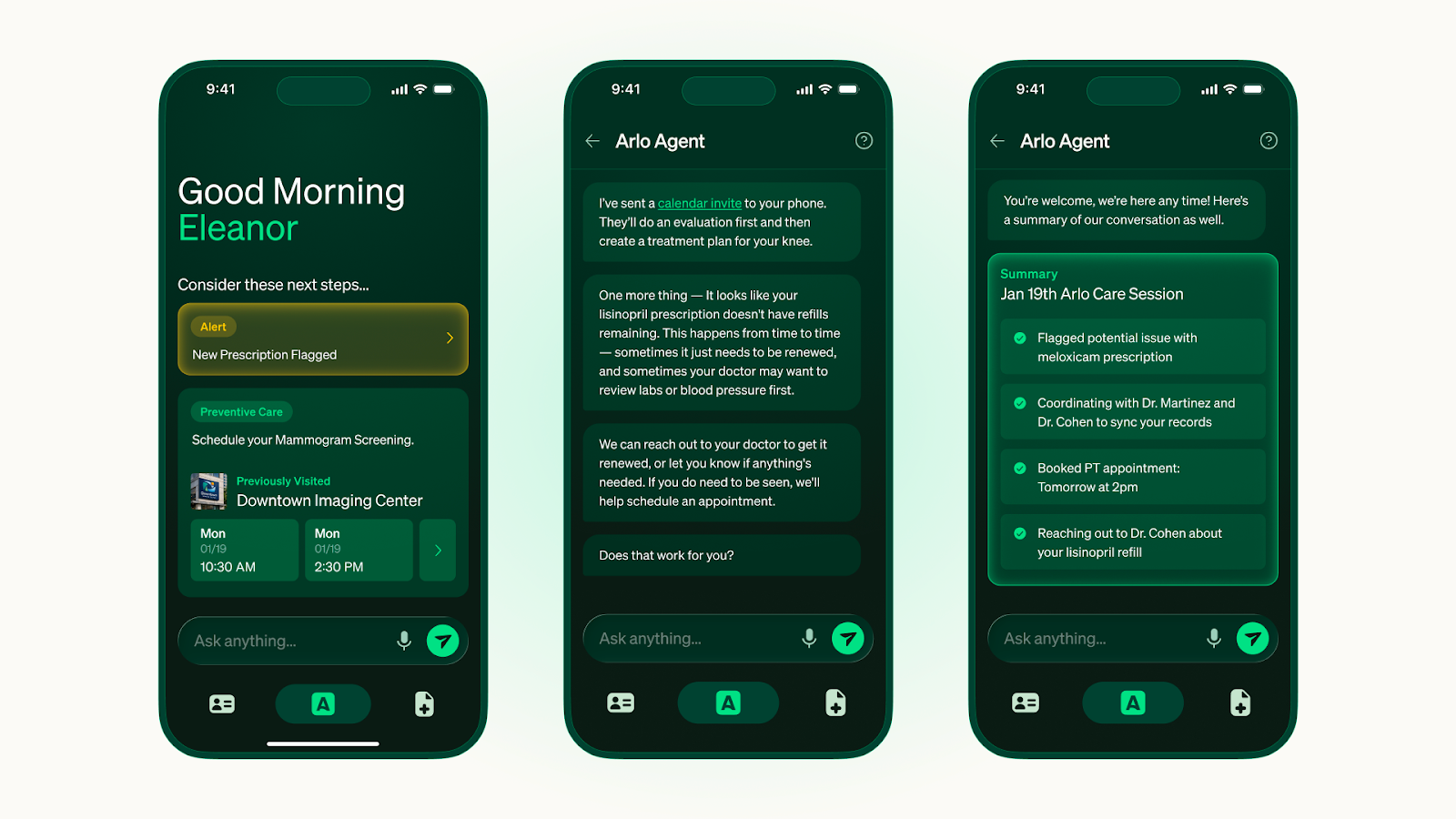

What Does Arlo Do?

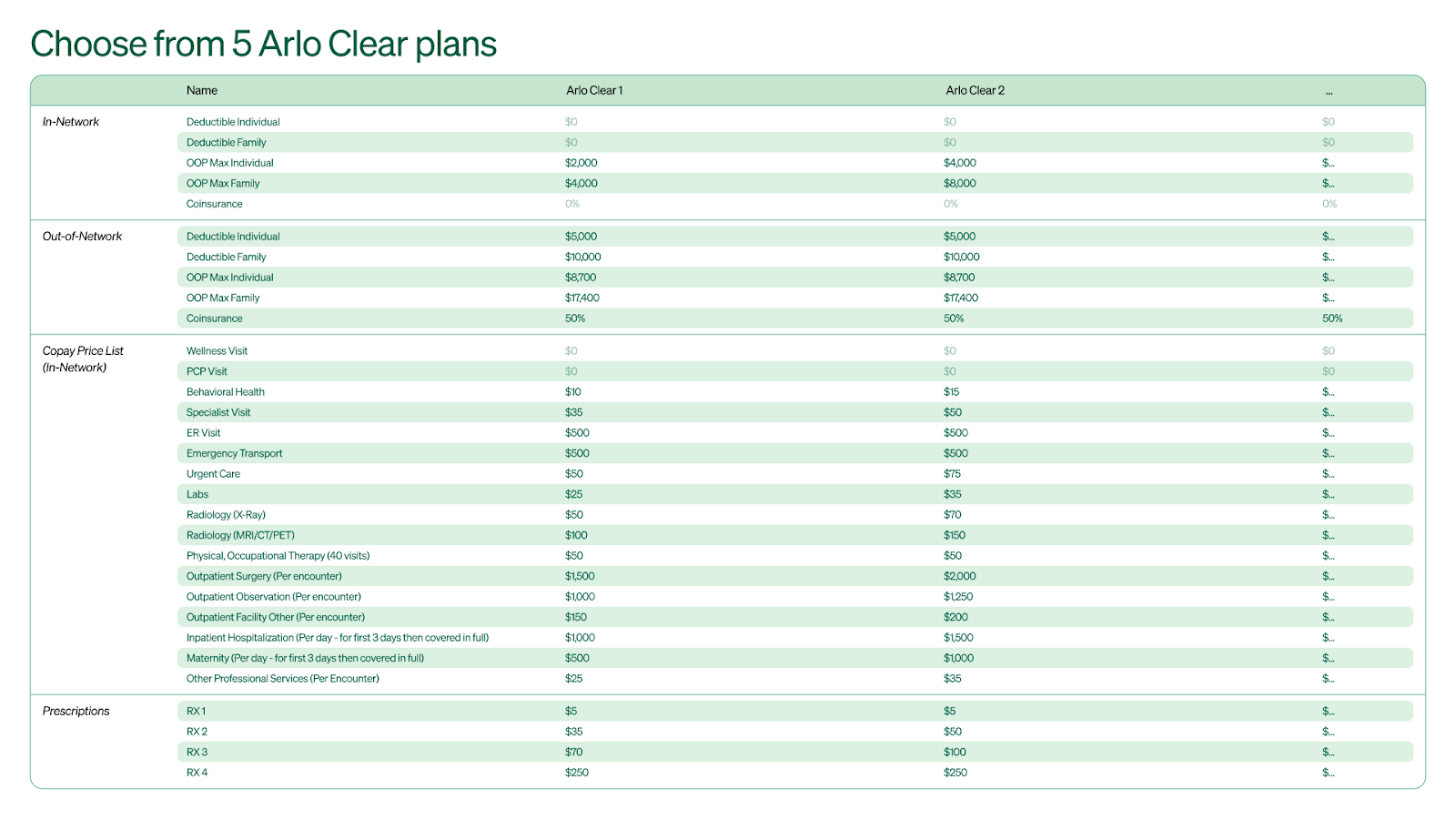

Arlo runs a level-funding plan for small businesses. Then they offer the employer a few different plans. All of their plans share the same core designs for patients:

- No deductibles or co-insurance for in-network care

- Patients are given guaranteed pricing for in-network care (even if something like a complication happens, they’ll get the guaranteed rate)

- $0 primary care visits

- “Millennial green” tones

They’re also going to be giving patients their own AI agent tool later this year. The tool will not only tell them about their plan info, but also schedule appointments on their behalf and ping their doctors for medication refills.

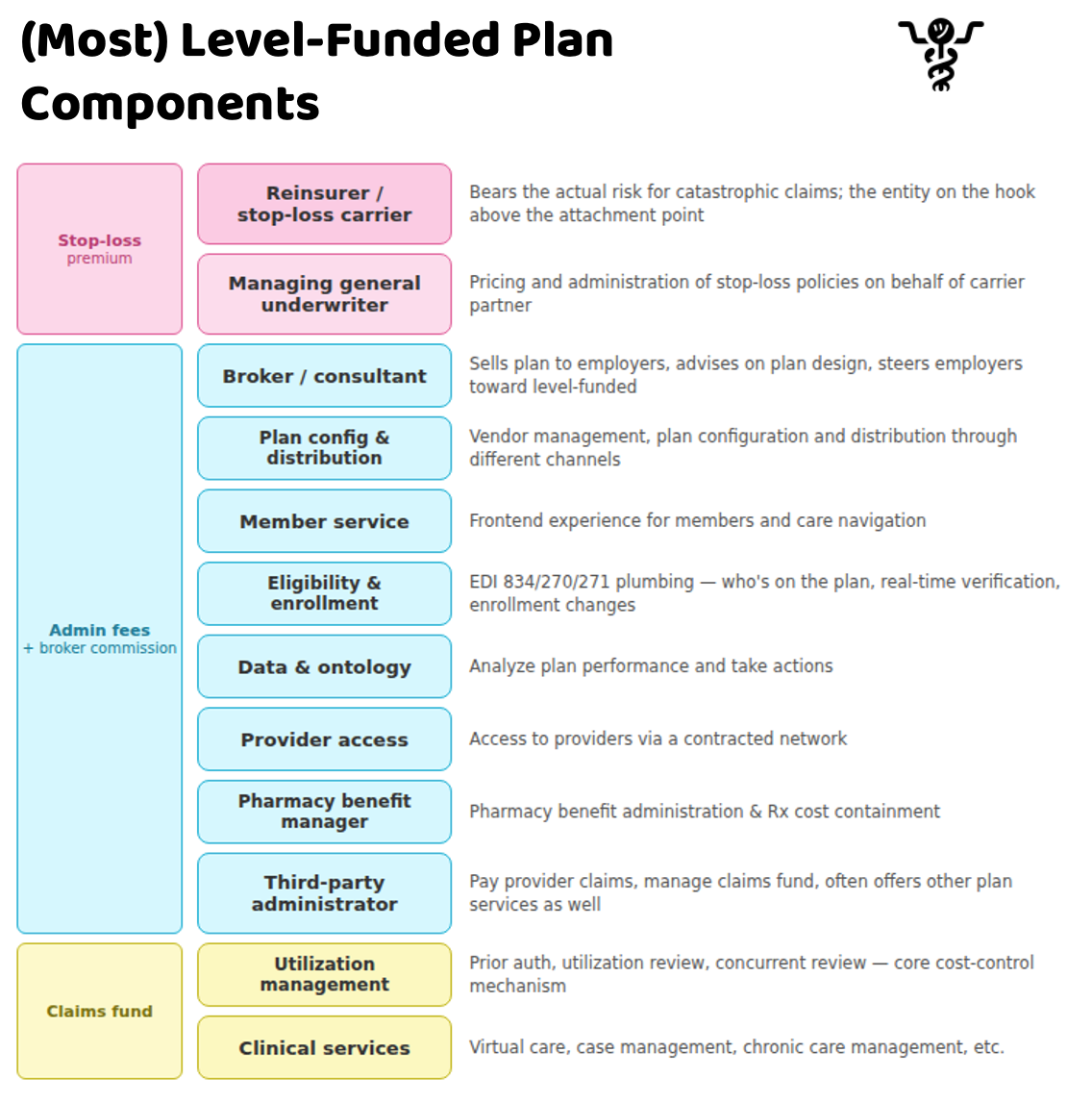

Arlo offers a tight number of plans and under the hood has built their own in-house products and integrations with a bunch of vendors for its different components:

- Underwriting groups and providing tools for brokers to give quotes

- Underwriting and issuing stop-loss insurance policies for groups.

- Managing contracted rates with providers (in-network and out-of-network)

- Pharmacy benefits, coverage, and finding which pharmacies are in-network

- Care navigation

- Paying claims out to providers

Underwriting is where Arlo started and a key part of the strategy. Owning underwriting and being able to issue stop-loss themselves means they can immediately reprice premiums when they roll out cost containment programs. Other health plans have to argue and justify it with the third-party stop-loss MGUs to adjust their rates.

Other level-funding plans also offer various levels of customization for each part of the plan and charge fees for each component. For example, when an employee sees an out-of-network provider, the level-funding administrators will negotiate the bill down. But then they charge a percentage of the "savings" as their fee. So if they knock a $10K bill down to $6K, they might take 30% of that $4K "savings." The employer ends up footing that bill obtusely.

Arlo’s bet is to offer higher and more consistent per employee per month fees but without the random fees that the employer can get charged in the backend. And at the end of the year, if the actual costs employees incur is lower than that claims fund, they get a 100% refund on whatever wasn’t spent.

What Is The Business Model And Who Is The End User?

Arlo has three categories of users:

Employers - The final buyer of insurance for employees. Their average group size is around 20 employees. They serve everything from daycare centers to VC funds to adult day cares (which aren’t the VC funds) to manufacturing. Anyone that’s >20 employees and offers health insurance to employees is a target employer.

Brokers - This is their primary distribution channel. Arlo built a platform that makes it easy for brokers to get quotes quickly and implement plans.

Members - Employees are the end users. Employees get the Arlo plan, and use the member app for care navigation, prescriptions, provider search, etc.

Arlo makes money in two ways. The first is as a Managing General Underwriter on behalf of large national insurance carriers (e.g. Nationwide) who offer stop loss insurance. Arlo earns commission and admin fees from these carriers for underwriting and administering the policies. They have fees at risk, so they better hope they get the underwriting right.

They also collect Per Employee Per Month fees from employers for administering the plan. This is for everything from offering AI navigation to administering claims, handling pharmacy, and everything people expect their health insurance to do.

Job Openings

Arlo is hiring for:

· Head of Engineering

· Product and Applied AI Software Engineers

· Sales Ops Lead

· Marketing Lead

Out-Of-Pocket Take

A few things I think are interesting about Arlo:

Innovation for small business coverage - The small group insurance segment hasn’t seen a ton of innovation, and frankly seems to be written off by most payers. Level-funding is new, more flexible, and provides products to an underserved market. It’s one of the fastest growing insurance segments for this reason.

In general, I think we need more innovation and experiments on the payer side of things, and level-funding for small employers is a great sandbox for this.

Payers offering consumer AI tools - As AI care coordination and primary care gets better, everyone is trying to figure out who should pay for it. It makes sense to me that payers would accrue a lot of value from people being able to access cheap navigation and triaging tools for free. If a payer told you that you could get a good or service for free with certainty, you’d probably believe it and be more likely to go there.

Today, Arlo is starting with care navigation and understanding benefits. You can imagine it being easy to start layering on AI primary care and triaging. When you control the payment rails, you have way more flexibility to cover them as these new technologies launch.

Asset light - Arlo has the benefit of being in the payer space but not taking on the full financial risk. They act as a coordinator and take on the parts where software can play a meaningful role (e.g. underwriting, navigation, etc.). But they outsource the operationally heavy stuff: TPA, network, and PBM. The financial risk on claims is largely held by the employers and stop loss carriers. They take some risk if they underwrite incorrectly, but that's a much more bounded risk than holding a balance sheet full of medical claims.

For a company trying to scale, this gets you a lot closer to software margins than traditional insurance.

–

As with any company, there are challenges:

The risk of underwriting incorrectly - Arlo underwrites the risk of employer groups on behalf of national reinsurance carriers, who pay them for that expertise. The reinsurance carriers are the ones who foot the bill based on Arlo’s underwriting. To make sure they have some skin in the game and so that they don’t underwrite bad groups, Arlo puts their fees at risk.

This means Arlo has to get their underwriting correct, or they’re going to lose money. They’re making a bet that their underwriting is accurate; otherwise, they’ll be underwronging. Yeah I’ll leave, sorry.

Incumbents could squeeze them - Large carriers like United and Aetna have their own level-funded products. They could afford to lose money on pricing temporarily to keep new entrants out. Currently the major carriers are bleeding on their government programs like Medicare Advantage and Managed Medicaid, so they likely won’t compress their margins on this segment in the near future.

But that could change, or they could view level-funding as an area to invest in more BECAUSE of the existential issues they face with the government-sponsored plans.

The ideological question on small group insurance - Level-funding is not legal in some states. The reason is because it enables employers with “healthier” pools to get underwritten at a lower rate, and then they exit the regular small group insurance market. If all the healthy small groups leave, that means the remaining small employers will have more costly employees, and it’ll become untenably expensive.

Health insurance risk pools work because the less costly people pay to subsidize the more costly people. The level-funding ethos is that employers with healthier employees are getting the short end of the stick in that bargain, and it enables employers to be more activist in lowering their healthcare spend.

There isn’t a “right” answer here, but each state has a different ideology around this and the regulations reflect that. It’s possible that as more products try to skim the healthier risk pools from the small group segment, that regulation will change and make it more difficult for level-funded plans to exist.

Conclusion

The small group insurance market is in a tough spot right now. Premiums are spiking, companies are already facing increased costs on other parts of the business, and they’re trying to figure out if they should offer coverage to employees at all.

There’s a longer conversation to be had about whether underwriting arbitrage is making the risk pool worse, and we’ve talked about this in previous posts. The answer is probably yes, but solving that requires a total rethink of how we allow businesses to offer coverage.

We need more experimentation on the payer side of things, and the small group market has been unloved here. Level-funding is new and where more of the action is. It’s exciting to see new players like Arlo bringing tech to this slice of healthcare. Arlo's bet is that employers and patients will choose them because of certainty: predictable fees, guaranteed pricing, and simpler plan design.

Maybe we can learn something from their plan designs if they’re successful and bring it to other insurance markets. I’ll be watching closely.

Thinkboi out,

Nikhil aka. "Jack Arlo" aka. “Setting the Barlo”

Twitter: @nikillinit

IG: @outofpockethealth

Other posts: outofpocket.health/posts

If you’re enjoying the newsletter, do me a solid and shoot this over to a friend or healthcare slack channel and tell them to sign up. The line between unemployment and founder of a startup is traction and whether your parents believe you have a job.

Interlude - Apply to Ship It! And Healthcare 101!

See All Courses →Don’t forget the application for our SHIP IT, our healthcare software engineering conference IS LIVE.

If you write or deeply work with code, have some experience working in healthcare, and want to has out how everyone is building things…you should apply to this. It’s small, intimate, and you’ll learn a lot.

And if you feel like you really need to get up to speed on how healthcare works, then you should let me teach you at Healthcare 101 starting 7/13!

This is for anyone hiring teams of non-healthcare people that need to get up to speed quickly (in 2 weeks) - we do group discounts too hit up ya boy. You’ll even learn how to make memes.

Get Out-Of-Pocket in your email