Value-Based Care Providers Need Their Own Insurance

Get Out-Of-Pocket in your email

Looking to hire the best talent in healthcare? Check out the OOP Talent Collective - where vetted candidates are looking for their next gig. Learn more here or check it out yourself.

Hire from the Out-Of-Pocket talent collective

Hire from the Out-Of-Pocket talent collectiveHealthcare 101 Crash Course

%2520(1).gif)

Featured Jobs

Finance Associate - Spark Advisors

- Spark Advisors helps seniors enroll in Medicare and understand their benefits by monitoring coverage, figuring out the right benefits, and deal with insurance issues. They're hiring a finance associate.

- firsthand is building technology and services to dramatically change the lives of those with serious mental illness who have fallen through the gaps in the safety net. They are hiring a data engineer to build first of its kind infrastructure to empower their peer-led care team.

- J2 Health brings together best in class data and purpose built software to enable healthcare organizations to optimize provider network performance. They're hiring a data scientist.

Looking for a job in health tech? Check out the other awesome healthcare jobs on the job board + give your preferences to get alerted to new postings.

TL;DR

Providers in value-based care arrangements take on financial risk. There are several different things they need to have to protect themselves financially and understand how they’re performing in a given value-based care contract. Today we walk through some of the financial products value-based care companies, including what surety bonds and stop-loss insurance do (with examples).

Paramean is a “financial risk” one-stop-shop for providers in value-based care contracts. They help design the contracts, have a software product to see how costs are trending, and provide those different financial products above to smoothen risk. We walk through the product, talk about what’s interesting about it (taking on financial risk) and where the tough parts might be in the future (e.g. pullback on value-based care).

For OOP readers, they've agreed to do a complimentary 30 min call for anyone in a VBC contract that wants a read on their risk structure. You can schedule it by emailing admin@parameansolutions.com.

—

This is a sponsored post - you can read more about my rules/thoughts on sponsored posts here. If you’re interested in having a sponsored post done, let us know here.

Company Name - Paramean Solutions

Paramean Solutions help value-based care providers underwrite their contracts and get financial products like insurance, surety bonds, etc.

The company is called Paramean which I think is just…combining parameter and mean. Listen, actuaries are creative in spreadsheets, they don’t need to be creative everywhere.

The company was founded by Isaac Edrah, did a lot of actuarial/financial risk work for VBC companies. Now he’s out for vengeance…by building tools to make it simpler for value-based care providers.

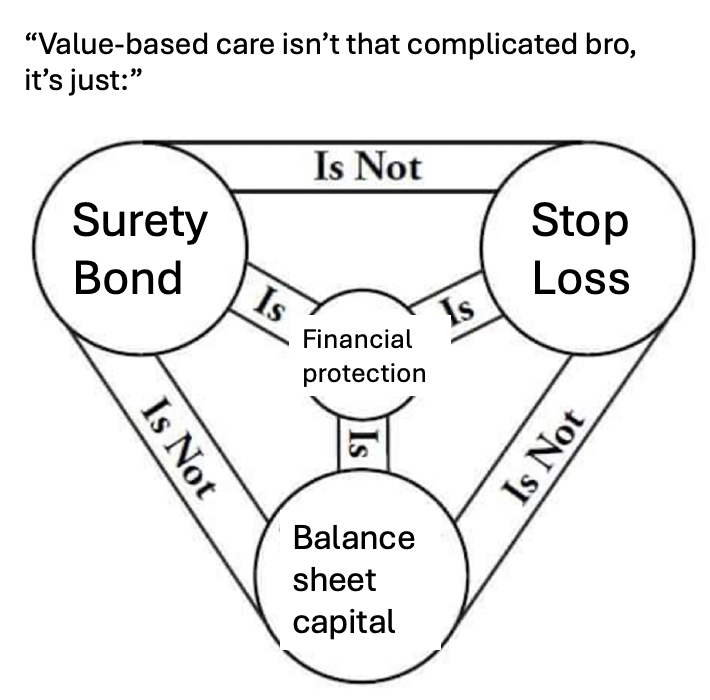

Some financial layers in value-based care

Today we’re going to learn at a high-level how some of the different financial layers of value-based care work. I can’t believe someone paid me to write about attachment points - I’m living someone’s dream and nightmare.

At the simplest, a provider that delivers care to patients has some sort of contract with a payer (the government, a health insurance company, an employer, etc.). In that contract, if the provider improves patient outcomes they get bonus payments. If they do poorly, they get penalized. There are lots of versions of this, which we’ve talked about previously.

But there are two issues.

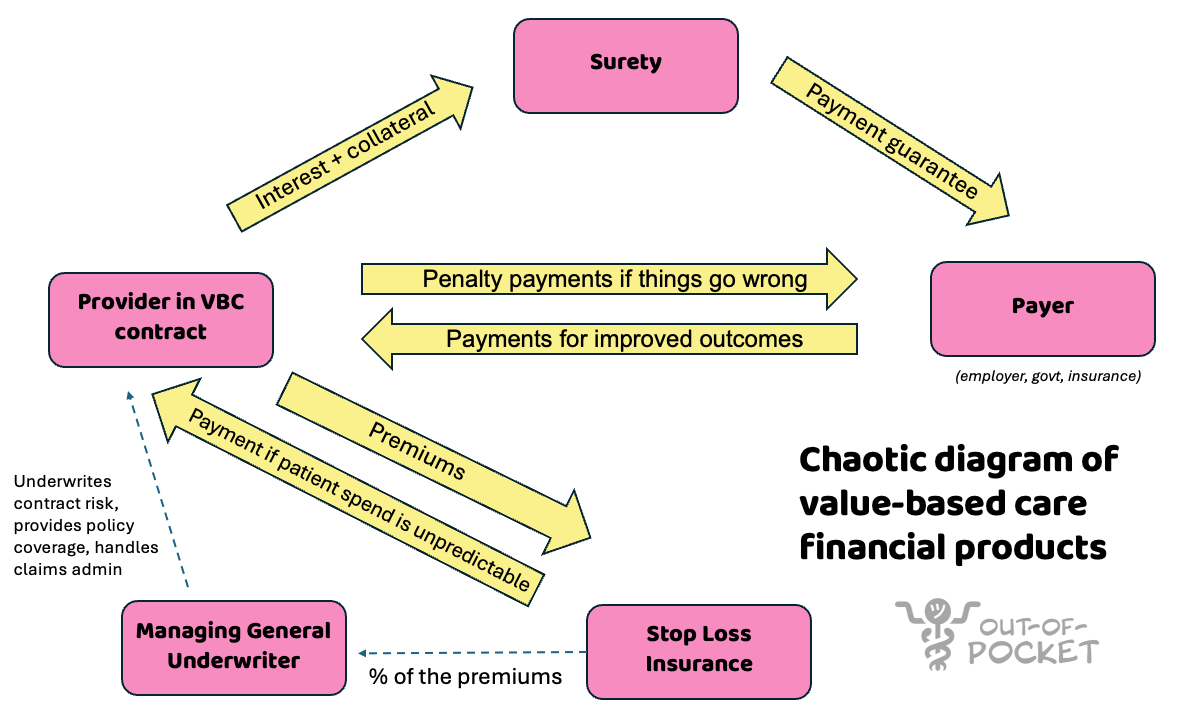

First, let’s say a provider has a value-based care contract with downside risk. The payer on the other side is worried the provider might not be able to pay any settlement the contract requires (shared losses / deficits). So the payer may require proof of financial security. This could be cash in an escrow, a letter of credit from a financier, or something called a surety bond. While this sounds like a Jonas Brothers pledge, a surety bond is a third-party company that guarantees to the payer: if the provider doesn’t pay, the surety will. If the surety pays, it has the right to recover that money from the provider over time.

And if the surety doesn’t pay, you’ve seen the Sopranos right?

Example: A provider signs a shared-risk deal with a $10M maximum downside. The payer requires a $10M surety bond. The provider goes to a third-party surety, which looks at the provider as a medium credit risk. They charge the provider 3% of the bond value per year in premiums ($300K/year) AND require them to stash $1M in cash collateral with them.

Now let’s say the provider goofs, does a bad job taking care of patients, and now owes $7M to the payer. The provider can’t pay, the payer can collect from the surety. The surety will collect back a fat stack from the provider revenue in the future to recoup.

Second, the provider is worried one of their patients might unexpectedly get really sick and expensive. Or something will happen that causes a lot of their patients to become expensive at once (e.g. COVID). If the provider is taking on a lot of financial risk on those patients, that could put the provider in the hole, no glory.

Because of this, they’ll usually buy something called stop-loss insurance. This will cover some of those costs above a certain amount (called an attachment point), either for an individual patient and/or the whole book of patients.

Example: A provider group is in a downside VBC deal and buys specific stop-loss with a $250K attachment point per member per year. If a member goes above $250K in spend, the stop loss will cover it. The stop-loss carrier charges $8 per member per month. for this coverage.

Now one patient gets extremely sick and racks up $1.1M in claims that year. The stop-loss policy reimburses the provider for the costs above the attachment: $1.1M − $250K = $850K

Or the provider will buy aggregate stop-loss that kicks in when total annual claims exceed 110% of expected, making David Goggins proud. Their expected total cost for the year is $100M, so the attachment is $120M. The stop-loss might cover 100% of everything above that amount.

Let’s say shit really hits the fan and the claims cost is ~$120M. Instead of the provider instead of paying $20M back to the payer, they will pay $10M while the stop-loss provider will cover the other $10M (for a premium of ~$500K/year).

These are all interlocking pieces that are pretty complicated!

What is the pain point? What does Paramean do?

If you’re a value-based care provider that wants to grow or scale, you need to have predictable control of your costs. A few really expensive unpredictable tail events can totally throw your entire financial risk out of whack. And the less predictable your finances are, the less likely you’ll be able to plan for growth, find partners for that growth, love, etc. This is why you get all of those financial products above.

However there’s a few issues with the current financial set up for value-based care providers The surety, the contract, and the stop-loss insurance are very intertwined but typically aren’t designed with the others in mind.

The foundation is the contract design - which is very complicated for providers on its own. How much financial risk should a value-based care provider take on? What patients are they on the hook for? Is anything carved out? This will influence the financial risk a provider is exposed to.

Then the surety and stop-loss serve different functions. The surety bond is underwriting the credit risk of the provider itself. This is to protect the payer. The stop-loss is underwriting the contract, medical risk, and patient panel. This is to protect the provider. You best protect ya neck.

These are typically done by different entities, are negotiated separately, and are typically done independent of a value-based care contract instead of influencing the contract design itself.

Paramean is a “financial risk” one-stop-shop for providers in value-based care contracts. The idea is by working on all of these things together, you can design the contract and underwrite the other products with all of the financial risks in mind.

For example, if you know the stop-loss is already underwriting the medical tail risk, then the surety doesn’t have to price as if there’s no other financial protection. This is one of the reasons surety bonds require a lot of collateral. However if it’s secured with the stop-loss for medical risk, then the surety bond can require less capital.

Paramean has a 3 different products with this in mind:

1) Paramean Consulting. At a baseline, setting up value-based care contracts is confusing. They have actuaries that help design and negotiate value-based care contracts with the payers and assess the baseline costs, trending costs, etc. in your patient population. This is the *whispers so the VCs can’t hear* services part of the business.

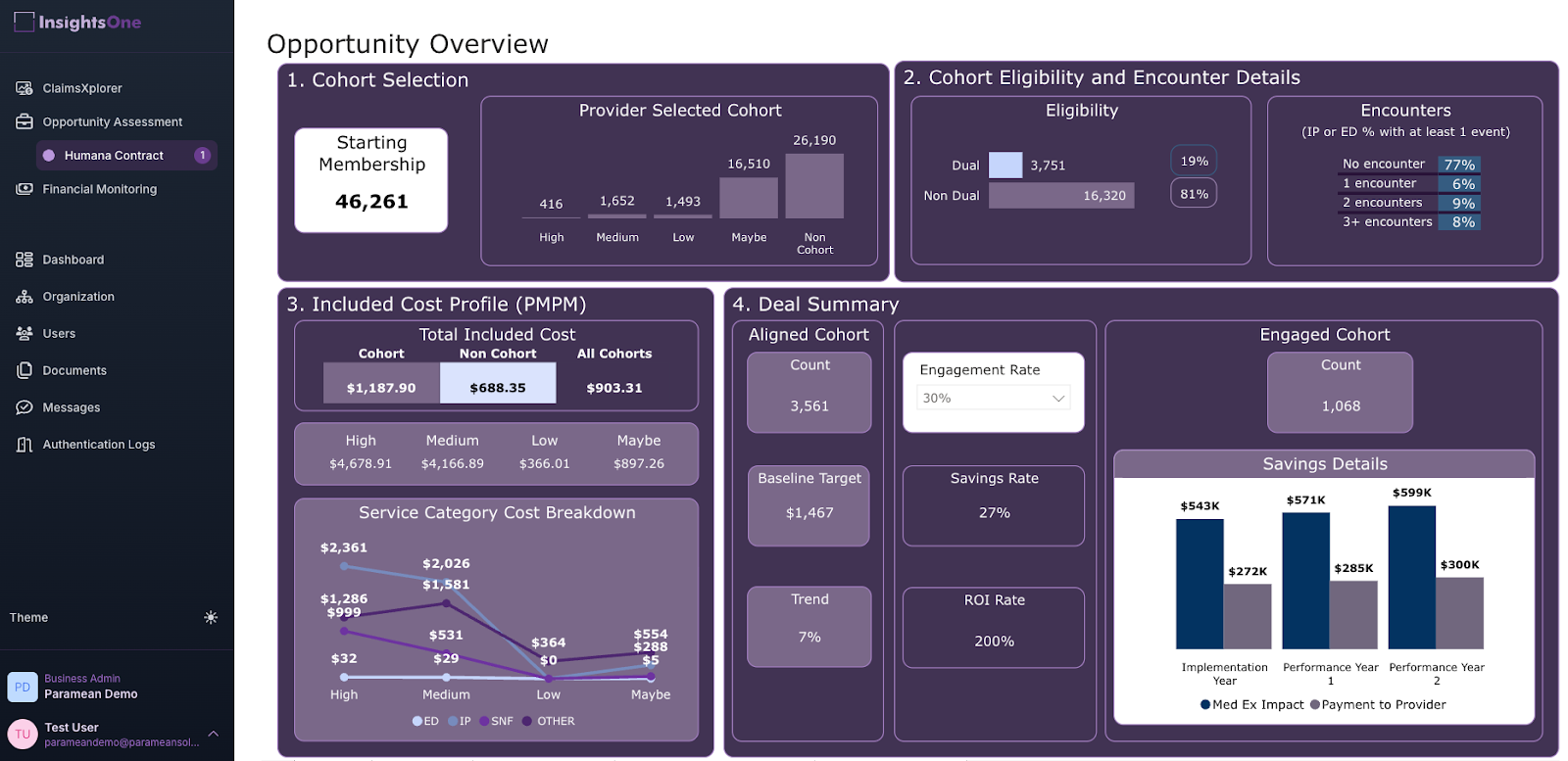

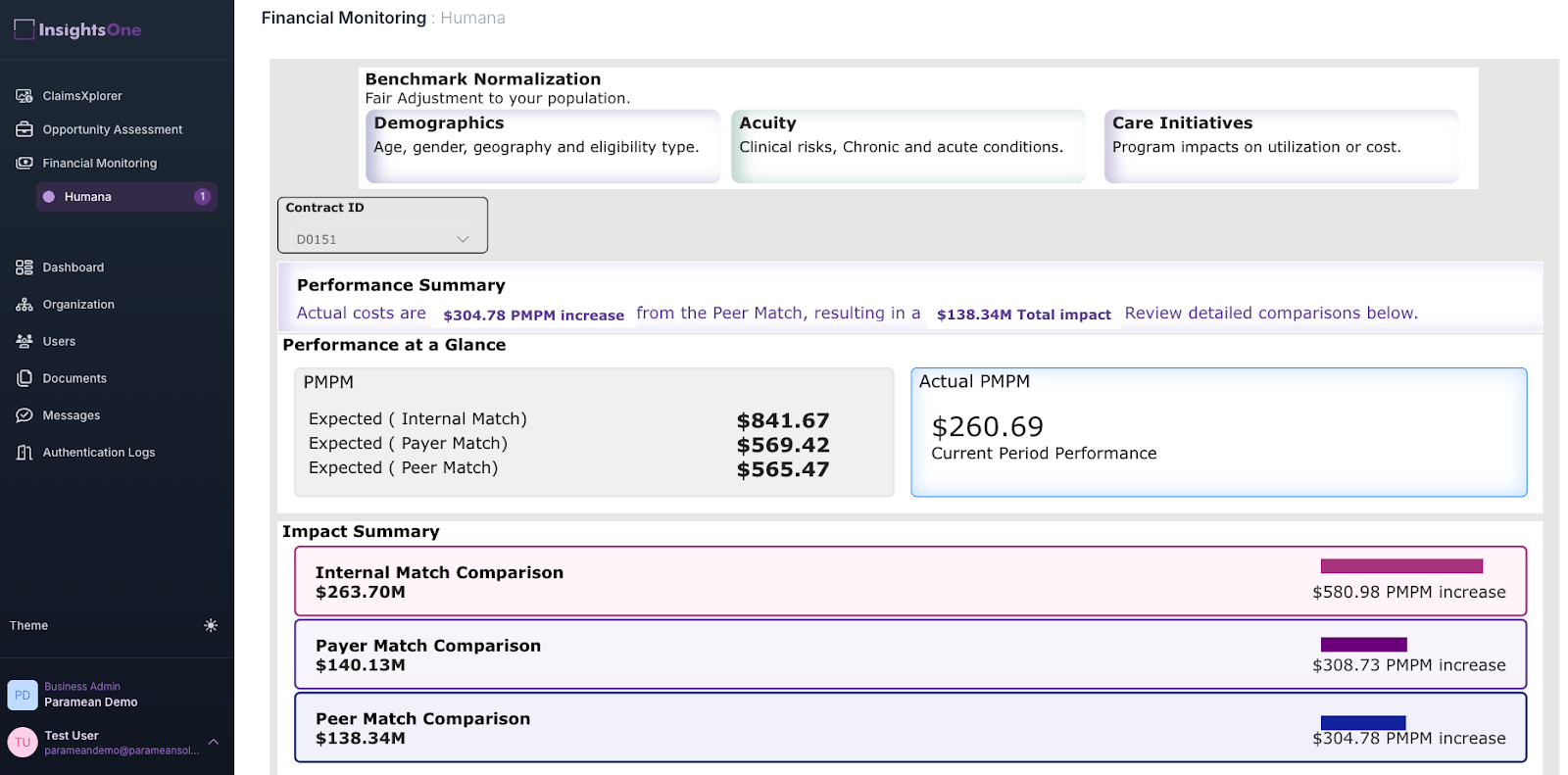

2) InsightsOne™ - Actuarial + AI platform. They have the InsightsOne™ platform. This takes in claims data, structures it, and then spits out dashboards that are relevant to the different value-based contracts a provider is in. How is the provider's spending trending? Which cohorts are particularly high spend? What is the spend forecast looking like? Machine learning under the hood identifies patients that might become high-cost and predicting future spend. And they’re making a bet that new AI models can help with underwriting and designing contracts.

This productizes some of the analyses an actuary would do, and make it self-serve for the provider. They have embedded services that help get this dashboard set up and tools to help with capital requirement planning based on performance. Then you don’t have to talk to the actuaries. Just kidding FSA MAAAs ASAs we love you.

3) Bammo Shield - Insurance & Capital solutions. Paramean acts as a Managing General Underwriter (MGU). This means that they structure, price, and manage those financial layers like surety bonds and stop-loss insurance. They look at the amount of financial risk in the contract, the care model of the company + the disease area (musculoskeletal, severe mental illness, etc). and they price the stop loss insurance for that contract. The same provider with different contracts will have different stop loss rates.

The idea is that by having everything under one hood - you can influence the contract design, monitor the performance in the contract itself, and underwrite the financial products more granularly to that specific provider and contract.

What’s the business model and who’s the end user?

Paramean charges differently for each product line.

For the consulting and advisory services, they charge hourly rates or retained fees based on the project and the type of contract the provider is working on. For their InsightsOne platform, they charge SaaS fees for access to the platform.

For the BammoShield reinsurance product, they partner with reinsurers who normally provide stop-loss insurance. The reinsurers pay Paramean a % of premiums to do the underwriting.

The end user for Paramean is usually a CFO, Chief Actuary, or the exec overseeing VBC contracting at a value-based care organization. Some examples of scenarios a VBC provider would come to them:

1. A provider is new to taking on downside financial risk in the Medicare Shared Savings Program. They’ve only gotten bonus payments or shared savings in the past, and they want help understanding the opportunity of a new payer contract with more upside but also possible penalties.

2. Providers who are already in downside risk arrangements like ACO REACH, but they want protection against their downside risk because trend in their population is getting more unpredictable or they’re increasing the share of downside risk they’re taking.

3. Specialist VBC providers that focus on a population like serious mental illness, or patients with multiple chronic diseases. They want clean actuarial data to understand their contract performance and assess their financial risk.

Job openings

Paramean is always looking for people who are excited about the extremely niche world of financial products for providers in value-based care arrangements.

There’s like 20 total who talk about that topic after work, so if that sounds like you contact admin@parameansolutions.com.

Out-Of-Pocket Take

There are a few things I like about Paramean, yanamean?

All-in-one for a specific area - Paramean is trying to be the glue between a lot of different moving pieces of financial risk in value-based care. As value-based care arrangements themselves have gotten more complicated and providers are juggling multiple contracts at once, the underwriting for them gets more complicated as well. Paramean’s bet is that they can develop an edge by just focusing on just providers in value-based care arrangements working with them end-to-end from contracting to insurance.

Sharing the underwriting risk - Paramean acts as a Managing General Underwriting. This means the stop-loss insurance goes to them to underwrite groups and handle claims, but it also means that they take on skin in the game. If the stop-loss company has to pay out the provider, Paramean also pays a portion of their fees if there are losses for the provider.

Companies have talked for years about how tech enables better underwriting, but that only really matters if you’re taking on the financial risk of that underwriting. This is a grill, putting money where your mouth is.

Productizing consulting - A lot of consulting shops run very similar analyses between clients with the same need, and charge as if they’re doing it from the ground up. Many times you’re just paying for a poor associate to fiddle with the excel formulas and get the right hex codes for the presentation.

Paramean is trying to productize their actuarial consulting services into their dashboard products. This should theoretically help them scale up with more clients by using more re-usable pieces under the hood.

As with any company, here are some of the risks I think Paramean faces as a business.

Underwriting incorrectly - Sharing the underwriting risk is cool, if you’re underwriting well. A risk to Paramean is whether they have an edge in underwriting by owning the whole process, because if they’re wrong they’re cooked. I’m guessing I don’t need to explain to actuaries that there might be adverse selection on the companies that choose to use a new underwriter…right…

Luckily they do have some hedging in their financials, since they also get paid consulting + SaaS fees. Ironically the actuarial firms are not going to bet it ALL on underwriting. Or wait, is that not ironic?

The risk of doing it all - Handling everything under one roof (services, analytics product, underwriting) sounds great in theory. However there are entire companies that build expertise in just one of these areas at a time. Your competition becomes firms that are experts in each of those areas, can promise certain turnaround times, have more customers to point to, etc.

This strategy only works if you can do all of them well, but I get why they’re shooting for it.

Value-based care going out of vogue - One of the bigger existential risks is whether value-based care continues in popularity. There’s been a big push for value-based care arrangements since the Affordable Care Act.

But lately a lot of sentiment on value-based care has changed. Companies are finding it difficult to build business models, critics will talk about the fact that these programs rarely save money, and even providers in it find it difficult to keep up with all the changes and operational overhead needed to participate. Taking on downside financial risk in particular is hard for providers.

If less providers participate in value-based care with downside risk, the less need there is for products like Paramean. But another way this can play out is by pushing more providers into value-based care arrangements with downside risk, which are the only ones that seem to actually save money. If that’s the case, then the demand for stop-loss products will increase.

Conclusion and Parting Thoughts

Value-based care is hard, no doubt about it. As providers take on more financial risk, the surface area of what can go wrong also expands. Managing financial risk becomes a key part of the job, no guts no glory.

As the value-based care ecosystem matures, it makes sense that the tools they need to manage their finances and risk will need to be more specific to them. Paramean is taking a big swing to build this - let’s see if it’s a good risk-adjusted bet :).

For OOP readers, they've agreed to do a complimentary 30 min call for anyone in a VBC contract that wants a read on their risk structure. You can schedule it by emailing admin@parameansolutions.com.

Thinkboi out,

Nikhil aka. “Let’s get downside to business, to defeat the huns”

Twitter: @nikillinit

IG: @outofpockethealth

Other posts: outofpocket.health/posts

{{sub-form}}

If you’re enjoying the newsletter, do me a solid and shoot this over to a friend or healthcare slack channel and tell them to sign up. The line between unemployment and founder of a startup is traction and whether your parents believe you have a job.

Interlude - Apply to Ship It! And Healthcare 101!

See All Courses →Don’t forget the application for our SHIP IT, our healthcare software engineering conference IS LIVE.

If you write or deeply work with code, have some experience working in healthcare, and want to has out how everyone is building things…you should apply to this. It’s small, intimate, and you’ll learn a lot.

And if you feel like you really need to get up to speed on how healthcare works, then you should let me teach you at Healthcare 101 starting 7/13!

This is for anyone hiring teams of non-healthcare people that need to get up to speed quickly (in 2 weeks) - we do group discounts too hit up ya boy. You’ll even learn how to make memes.

Get Out-Of-Pocket in your email